Does the bank interfere with a charter party by foreclosing its mortgage on a vessel?

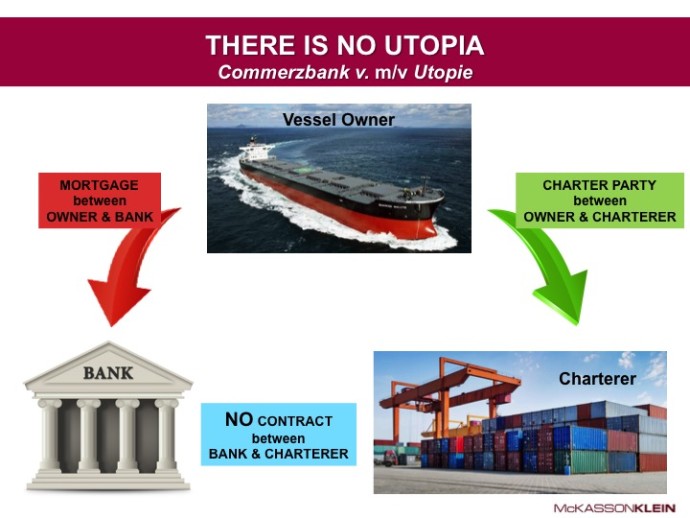

A ship mortgage is contract between a bank and vessel owner for a loan on the vessel, and a charter party is a contract between a vessel owner and charterer for use of a vessel. Different contracts, of course.

If the vessel owner defaults on payment, the bank can foreclose the mortgage, arrest the vessel in the US under a Rule C action (under a “maritime lien” theory), sell the vessel at a court ordered judicial sale and apply the proceeds to the debt. However, this leaves the charterer without a vessel under the charter party, and exposed to claims by cargo owners and/or sub-charterers.

The charterer’s problem is that while it can sue the vessel owner for breach of the charter party, since it does not have a contract with the bank, it cannot enforce its charter party rights directly against the bank. In a 2013 case in Louisiana, Commerzbank v. m/v Utopie, the charterer found itself in this exact situation. After the bank had filed its Rule C action and the vessel had been sold at judicial action and the proceeds placed into the court registry, the charterer filed a Rule B attachment action against the bank, seeking to attach the vessel proceeds from the judicial sale (as property of the bank, i.e. the debtor).

To get around the absence of contractual privity with the bank, the charterer (creatively) alleged a claim for “tortious interference with contractual relations” under German law as governing law, arguing the bank:

- Knew owners were in “dire financial straits,” but failed to foreclose

- “Effectively intervened” in owner’s management, aiding & abetting in its insolvent trading

- Allowed the vessel to sail to a suitable/attractive location, to foreclose the mortgage & file suit

- The foreclosure forced termination of the charter party, causing damages to charterers

- Should have waited until after the charter ended, before foreclosing the mortgage

Since Rule B is a pre-judgment remedy for security, the charterer did not have to prove the allegations were true to obtain the attachment order – it simply had to assert allegations that were prima facie valid (i.e. sufficient to support the cause of action), a low threshold. A federal judge granted the attachment order against the sale proceeds.

The case settled soon afterwards.

The lesson from the m/v Utopie is the power of creative lawyering and “out-of-the-box” thinking. It is possible the charterer may have been able to prove its claim under German law (assuming the US court agreed on that “choice of law”); but had US law (and maybe even English law) applied, it would have been difficult for charterers to prevail since an “interference with contractual relations” claim requires proof the bank induced the owner to breach the charter or the bank intended to interfere with the charter party. As long as the bank acted lawfully to enforce its own contract (mortgage), proving such a claim is unlikely.

The prima facie Rule B allegations were sufficient to obtain an attachment order and, as a matter of strategy, may have pressured the bank to settle.

Related content: